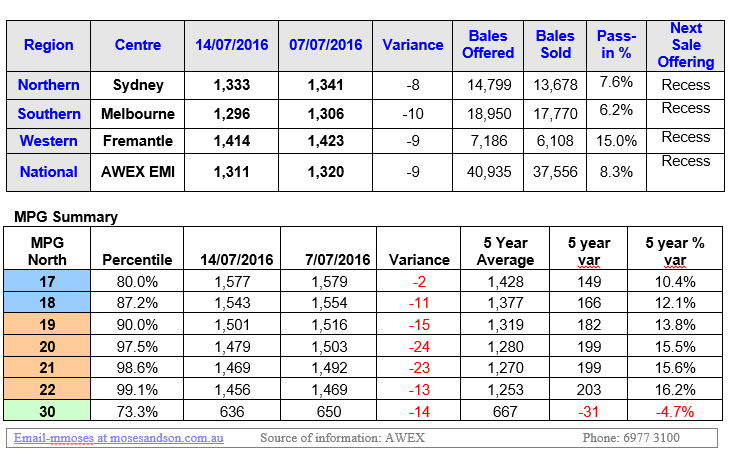

Wk 02 14/07/2016 Whilst the AWEX EMI failed to post its fifth successive weekly rise, the 9c fall was still an exceptional result for Australian Wool Industry. Closing on 1,311c the EMI in USD terms added 5c to close a 998 c US the highest USD EMI for 12 months.

The wool market sailed into a difficult week with the AUD breaking the 76USc mark. 40,935 bales were offered, slightly more bales than earlier predicted however it is not surprising the lure of appreciating prices at Auction drew bales from the hold cupboard.

The majority of the Merino fleece types posted falls between 10 to 25c for the week coming off an extremely bullish month of appreciating prices, whilst the 16-17.5 micron fleece types defied this trend posting stable and at times slightly dearer prices for the week. Skirtings bucked the fleece trend and held their previous week’s levels, before posting slight increases on the final day. Crossbreds were variable with the 25-26 micron types posting 30c increases whilst the 28 micron types held form and the 30-32 categories lost 10-15c, and last but not least, the carding indicators lost up to 5c for the week.

We now enter a very interesting time for the winter 3-week recess, with the YOY bales offered down an alarming 8.2% in Australia. There is no doubt that the past month’s rise is partly due to an increasing concern along the supply chain about reducing supply in Australia.

The result of 1,311c for the EMI and almost 1,000USc EMI presents amazing opportunity, for those wool producers who start looking at forward prices and what impact that may have on their income in the upcoming financial year.

Southern Aurora Wool traded 82,000 clean kilograms this week which is a fair indication that the Forward bids are palatable at up 5% discount to the current spot levels for 21 micron for Spring delivery. Hedging activity on the 19 micron contracts has seen some sellers taking a position in January 2017 at 1435c and January 2018 at 1430c a similar forward discount premium of 4.5%.

Whilst we do not know where we sit in the price cycle at the moment, we do know we are within 2% of the highest levels seen for the medium micron merino wool categories. We also know that looking back at historic price spikes, the average retracement from June-July to October is about 16-18%. The forward market is presenting opportunity to mitigate this risk for mid-September at 4% discount to the spot and for around -6-7% for mid-October, please consider. ~ Marty Moses

Market Report (PDF)