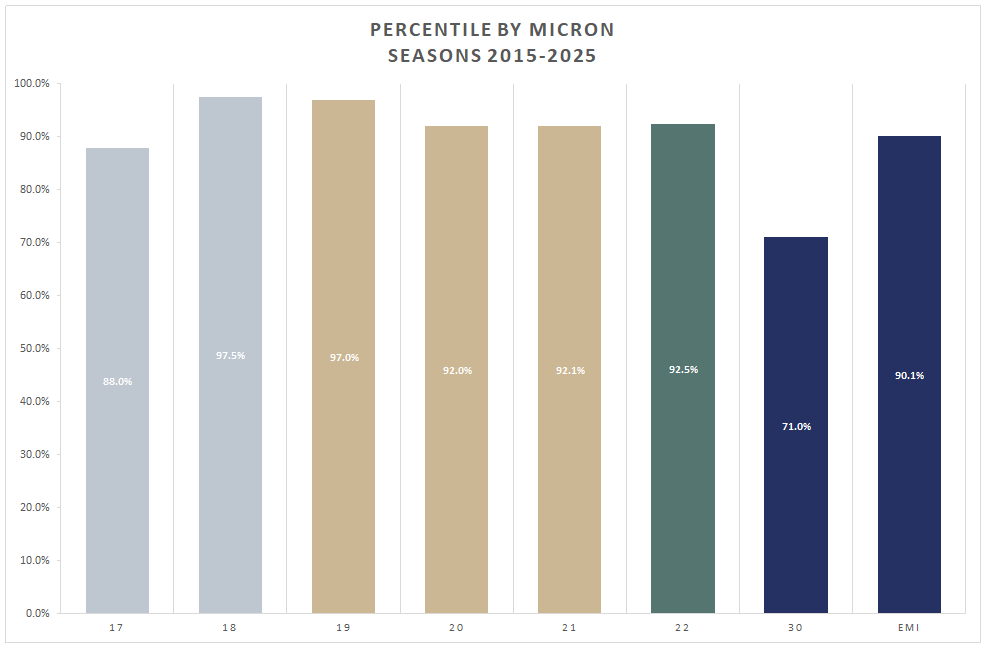

Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S43

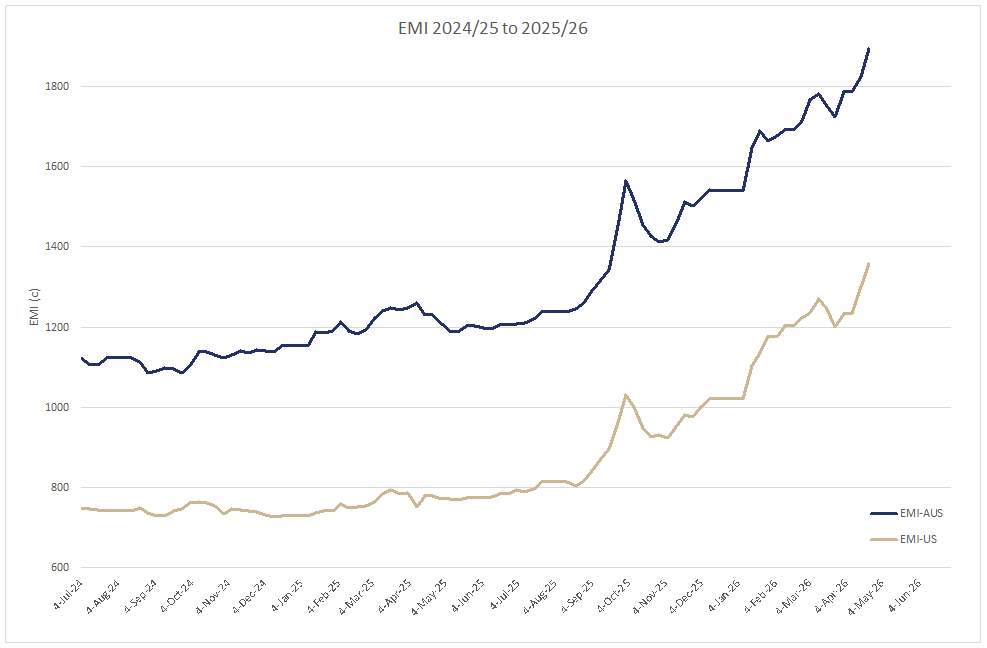

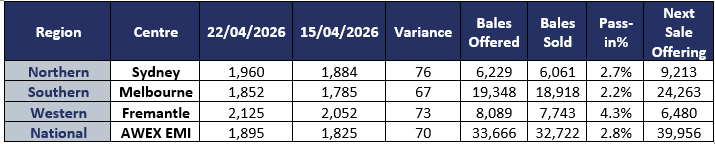

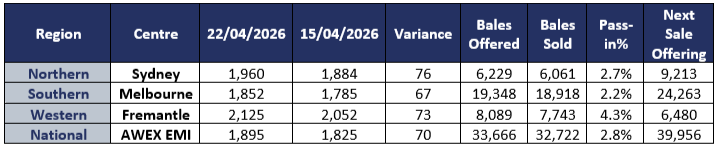

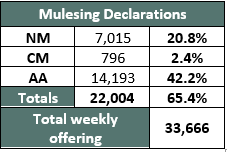

The AWEX EMI closed on 1895c, up 70c at auction sales in Australia this week. Whilst Melbourne and Fremantle offered on Tuesday and Wednesday, the volumes of wool offered in Sydney only constituted enough volume to offer on Wednesday. 97.2% of the 33,666-bale offering was cleared to the trade in what could only be described as frenetic competition on almost all lots offered. Currency exchange was not a factor in this weeks result, despite the exchange rate increasing slightly over the selling week.

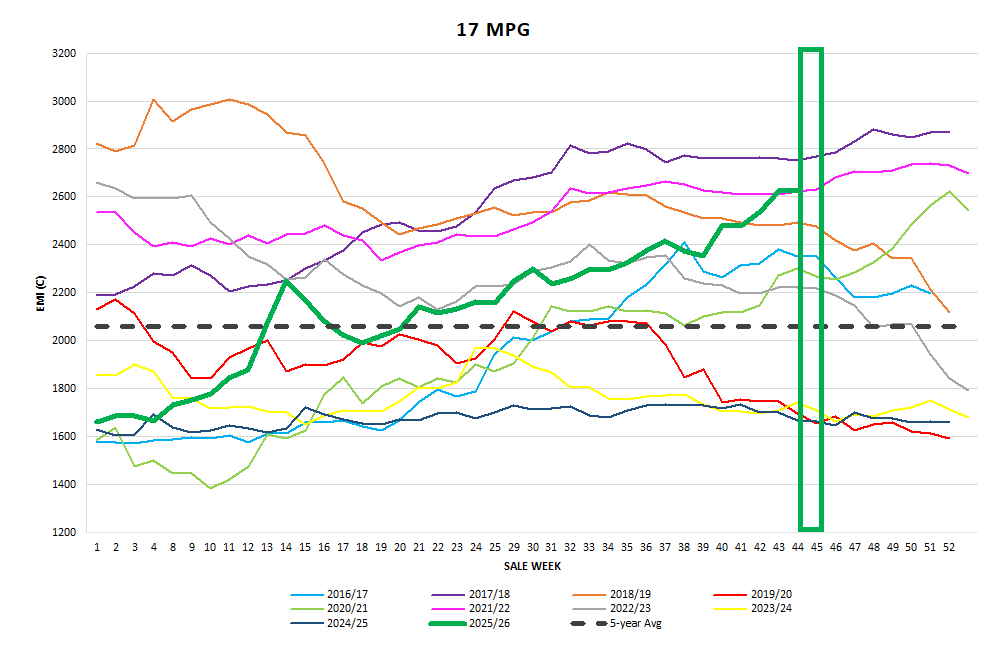

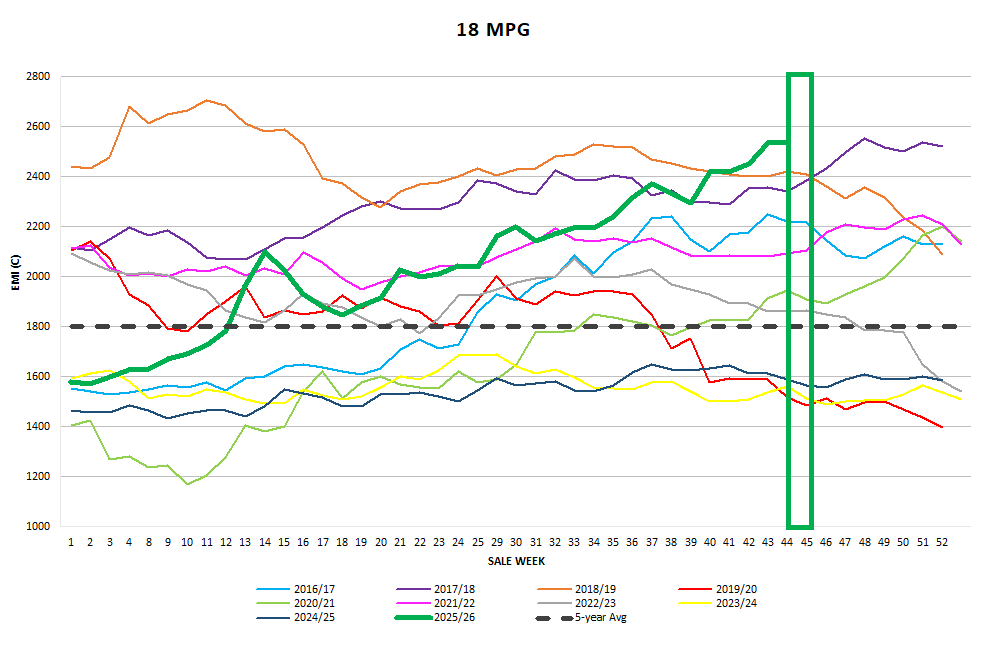

Merino Fleece

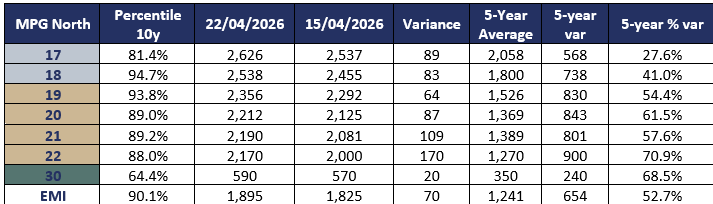

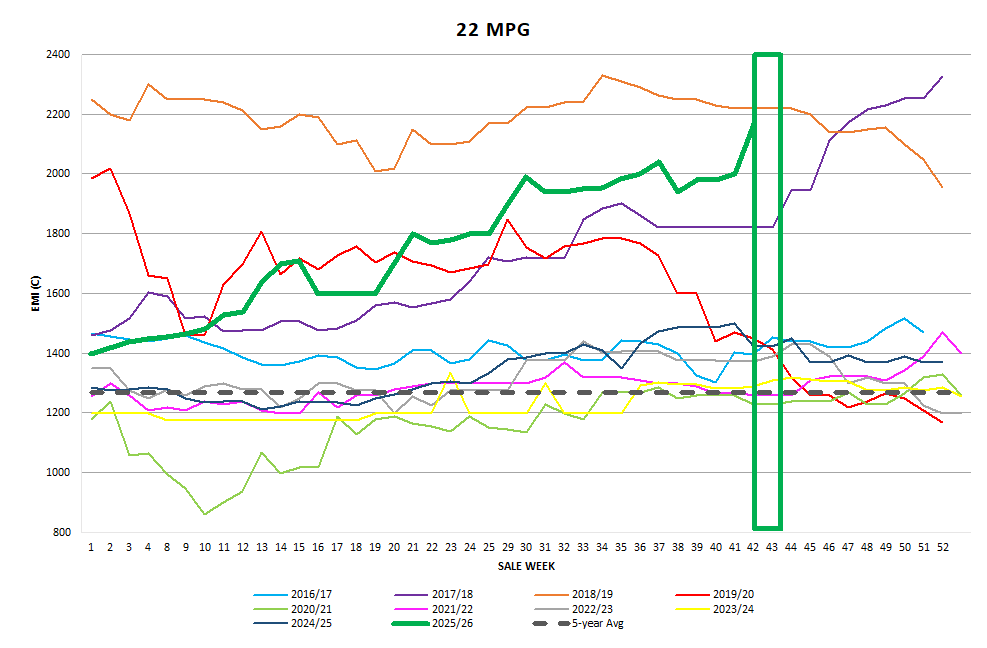

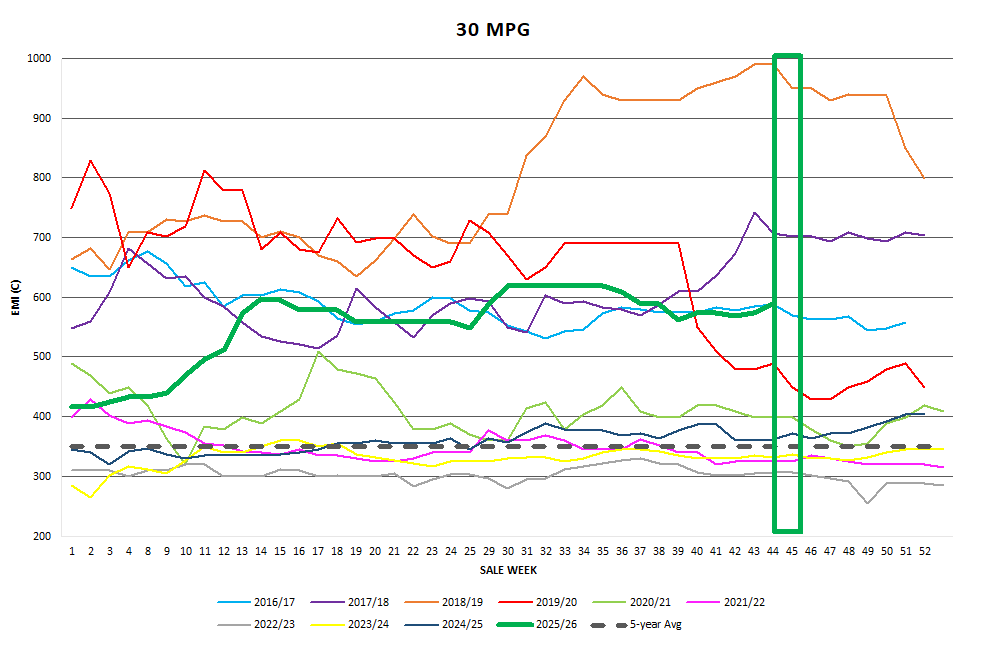

Merino Fleece led the market with rises in the MPG’s up between 64c and 121c in the Northern markets. Buyer sentiment seemed to be a ‘”Purchase at all cost” strategy with many companies struggling to secure the volume to satisfy their needs. With less than 2% passed in the Sydney and Melbourne Fleece offering, it left many exporters short at the end of the week. Competition came from the usual suspects, the large local traders and Chinese indents however this week saw some Chinese processors re-enter the market after a pause from purchasing. The top 4 exporters taking over 60% of the fleece offering. The 18 and 19 Northern MPG both moved into rare air this week achieving their highest price at this time of year in history while most other merino MPGs were not that far away.

Merino Skirtings

Merino Skirtings opened the week with solid price increases. Melbourne opened 30-50c clean dearer and added another 25c on Wednesday. Sydney opened on Wednesday up 50c with the best skirtings up to 100c dearer for the week. Competition like the M Fleece was a balance between the large local traders and Chinese indents with the top 4 buyers taking 65.4%

Merino Cardings

Merino Cardings continued to rise steadily adding 9c in Sydney and 27c in Melbourne. A selective oddment market rewarded bulky, stylish wool with 20c rises whilst poorly prepared, shorter length lots were slightly cheaper. Competition on the best bulk good, colour, FNF Merino Crutchings were absolutely off the charts.

Crossbred Fleece

Crossbred Oddments

Crossbreds

Crossbreds were also keenly sought after with Sydney experiencing a 77c rise for the 26 MPG largely driven by best specified fleece types. 28 MPG was also dearer adding 37c. The Melbourne offering rise between 4 and 21c probably reflecting the quality of the offering.

Next Week

Next week the offerings ratchet up to a solid 39,956 bales, no doubt the post easter market performance eking out wool tested in previous seasons from brokers stores. You can only sell it once!! The early market intel seemed divided between a retracement of 50c clean and an increase of 50c clean. We have an additional day to ponder which one theory we wish to believe, with the Anzac day holiday on Monday. Lest we forget! ~Marty Moses

Market Commentary

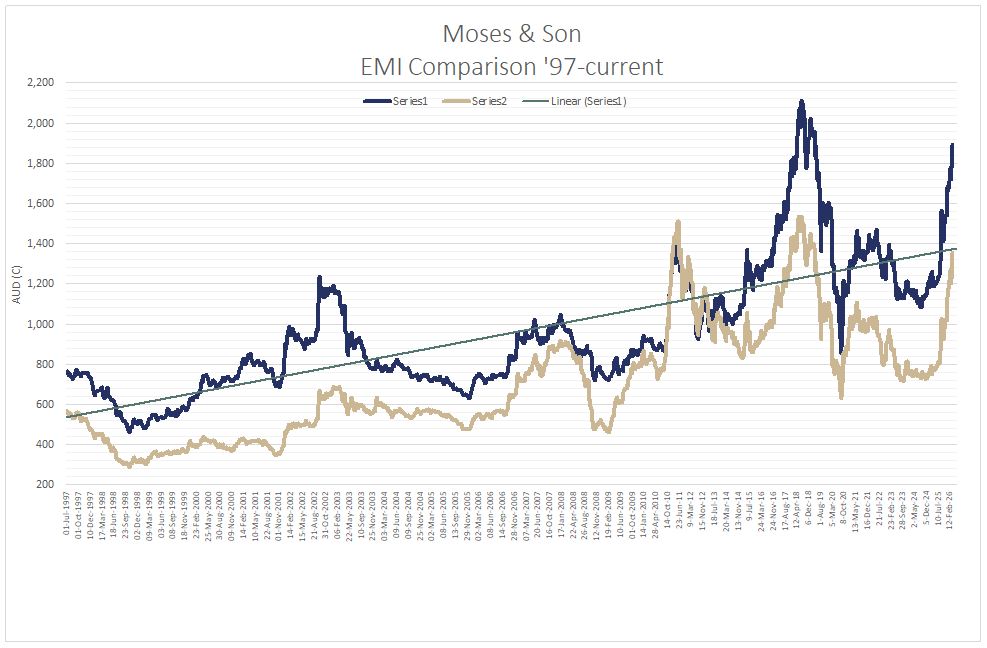

The Wool production forecast Committee released its forecast for 26/27 season today predicting production of 243.9mkg, down 4.5% from the 2025/26. Year-on-year, the EMI now sits 53.8% higher in AUD terms and 74% higher in USD, underlining the depth of demand supporting the market.

The key driver of the sharp price rises remain lower volumes of wool produced in Australia, but news emerging from the recent 48th Wool Salon held in China is, whilst the rest of the world retail sales are continuing to fall the news that demand in China is making a substantial recovery! Wool apparel demand in China is up 14%, whilst merino demand is up 20%. Whilst wool is now ranked in the top three most popular fabrics for Fashion and Activewear, the largest growth is in the “Outdoor Wool” which is reporting a 58% growth, whilst the “Merino Outdoor” garments are up 120%.