Week 43:

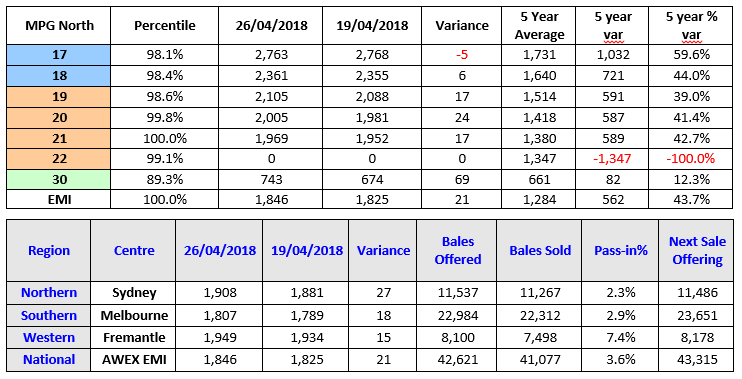

The AWEX EMI closed the week on 1846c – posting a rise of 21c and surpassing the previous record EMI of 1834c set in February this year. The current level is 23% or 345ac higher than at the same sale week of last year with 50,000 more bales sold through auction than at the same period last year.

The market selling days (split by Anzac Day on Wednesday) experienced two entirely differing emotions in what was an abnormal selling week. Tuesday saw the market race up 22c pushing the EMI to 1847c and seemed to be unstoppable. Conversely from the opening lot on Thursday, the market sentiment was weaker on the majority of Merino Fleece and Skirting categories as their resistance to Wednesday’s prices emerged. The market selling centres varied in price with Sydney maintaining Wednesday’s price levels much better than the Melbourne Market.

Whilst the Merino Fleece and Skirtings finished in positive territory increasing between 5 and 25c with the exception of the 17μ and finer categories.

Crossbreds continued to increase their price levels throughout the week and continue their 4 week bull trend. 25μ and 26μ MPG’s posted a massive 149c and 96c increases respectively and set new price records. The 28-30μ MPG’s increased by 67 and 69c respectively with the rises distributed over the two days.

The Cardings indicator increased 11c in Sydney and 8c in Melbourne, with the rises also spread evenly over both selling days. 42,621 bales went under the hammer with a pass in rate of just 3.6% reflecting the solid weekly rises in the market and the new EMI level achieved.

Forward Market Report– Michael Avery: Southern Aurora Wool

Another week of high volatility in both the spot auction and the forwards. The rise of Tuesday, fuelled by a lower Aussie Dollar, quickly turned Thursday. The strong bidding in the forwards all but disappeared as off shore interest failed to materialise as the week progressed. The need to keep machinery running is always balanced by the ability to pass the raw material price along the pipeline. This balancing act plays out by demand shifting between fibres, origins and microns. This is probably best illustrated by the basic changes over the last few months. To reduce the impact of the rise in prices we have seen the difference between 19 and 21.0 micron change from 350 cents to 130 cents since the Christmas recess. Similar shifts have been seen in the Crossbreds with 28.0 microns outperforming the finer microns as the price pressures impact merino demand. The current bull run in prices differs from previous peaks as it has continued relatively unabated for 24 months. This could indicate that the impact on demand reduction could be less than previous dramatic rises that have led to just as dramatic falls.

Commentary: The Wool Production Forecasting committee updated their report on the 2017/18 season this week with a down grading of 0.6% to 338mkg and the committee’s first forecast for 2018/19 of 333 MKG a further fall of 1.7%. This week, the sales from the auction totalled $80.6m and the YTD total value of wool sold is $2,848.91m. The positive market has attracted another solid 43,315 bale offering for next week. As we move towards the majority of volume producing MPG’s achieving best merino ever price levels, it is a reminder that, despite the prolonged dry period we are experiencing, it still remains a great time to be in the Sheep and Wool industry and now we can extend that catch phrase to the comeback and fine crossbred sector.

~ Marty Moses