Week 02:

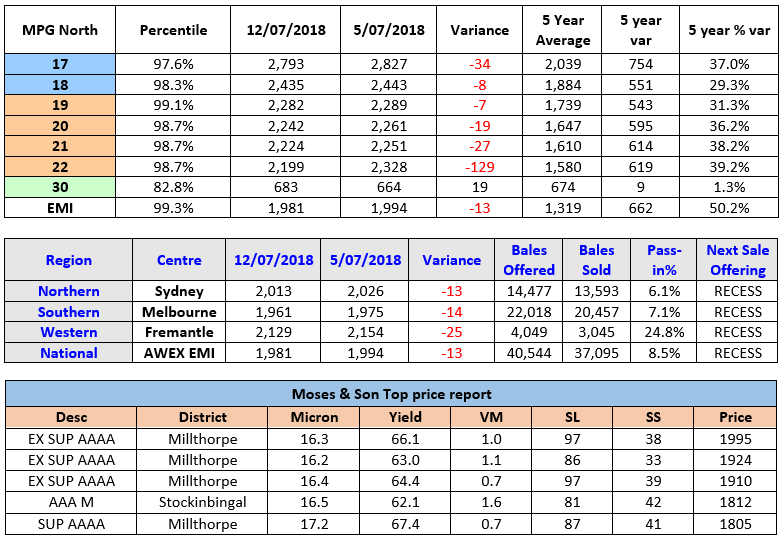

The AWEX EMI closed on 1981c – down 13c at auction sales in Australia this week.

The softer market seemed to find a level that traders and exporters were comfortable to purchase by midway through Wednesday’s sale. By Thursday, there were some more positive signs in Sydney with the NMI increasing 3c whilst in Melbourne the SMI fell 3c.

From the 40,544 bales offered, 91.5% was cleared to the trade which was heavily influenced by the West Australians passing in or withdrawing almost 30% of their offering on Wednesday. China remained dominant purchasers of Australian Wool, with their purchases for the past season totalling 223.6 Mkg (75%).

Merino Fleece generally lost between 5 and 35c, with the best support felt in the 17.5-19μ range closing 5-10c down. The heaviest falls were felt in the 17μ and finer, closing down 35c whilst the 19.5 and coarser posting 20-25c losses for the week.

Merino Skirtings were generally 10-20c with the heavier VM lost most affected and the 19.5μ and coarser skirts with less than 3% VM actually increasing in price for the week.

Crossbreds posted a mixed result with the lots finer than 29μ, falling 20-40c whilst the 30μ lots gained 10-20c. Merino Cardings were in short supply but failed to retain last week’s price levels, posting falls of 15-30c across the three selling centres.

Forward Price Report from Michael Avery (Southern Aurora Wool): The auction market closed for the recess looking to find a level. With buyers looking to clean up shipments prior to the break there was considerable variation in demand between micron and selling centres. The forward markets remained patchy with buyers and sellers alike finding it difficult to ascertain fair value. New forward business is difficult right at current spot levels. Downstream processors are having to deal with the disconnect between the current market for tops and yarn and the current replacement level. Spring traded for 21.0 September 2150 and October 2120. This would indicate that market is looking to return, in the medium term, to the May which averaged 2100 but with a wide range from 1970 to 2250. Bidding levels for summer and the New Year highlight the uncertainty as we move further into the new season. That said it was pleasing to see trades out in 2019 with growers achieving prices in the 90 to 98 percentile band. The growers hedging 21.0 microns for 12 to 18 months out are locking in prices that have been only been achieved 2 to 3 percent of the time in the last decade.

Scott Carmody (exporter) reports: The past few weeks have seen almost 80,000 bales sold to the trade and this has alleviated to some degree the pressure on access to supply for the time being for overseas manufacturers. Global stocks of wool and particularly the Merino quality for apparel is still dangerously low. We are in midst of the quiet period in retail for wool, i.e. the Northern Hemisphere summer, and we will need to wait a month or two before production needs to be ramped up to supply the upcoming peak period of fall and winter, and then the pressure will be exerted once more on supply.

Commentary: Despite the EMI slipping below the 2000c mark, the wool market breaks for three weeks holding its head up very high. The catch phrase “it’s a great time to be in Sheep and Wool” remains extremely real, and sheep and wool producers should be buoyed by the demand on their amazing products. The stats that were produced are amazing and will be released in a separate report over the next few weeks.

Moses & Son will be reviewing this market report over the month so if you have any comments or suggestions please forward them to mmoses@mosesandson.com.au ~ Marty Moses