Week 45: 10/05/2018

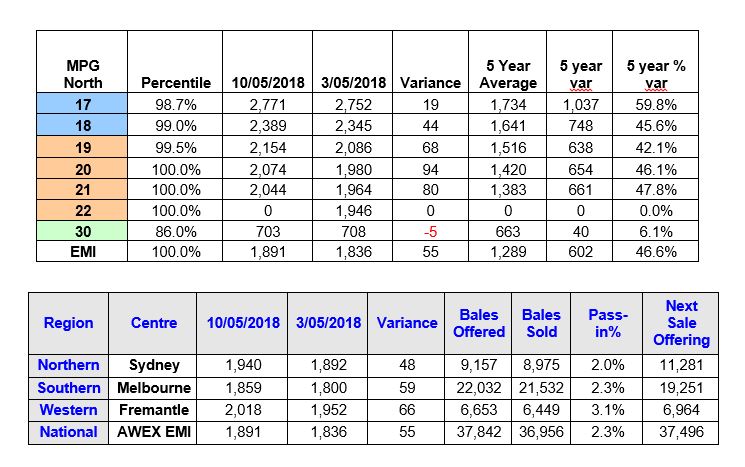

The AWEX EMI posted a 55c increase to close on 1891c at auction sales in Australia this week. The weekly increase in

the EMI was the largest since February this year, in addition it surpassed the previous record for the EMI of 1847c set

in April ‘18.

Merino Fleece of all categories received new interest and spirited bidding was the feature of the week as the “buy at

all cost” strategy pushed some MPG’s up over 90c for the week. The medium merino MPG’s (20-23μ) pushed to new

highs, in some cases 40c above the past records. The superfine and fine MPG’s posted good gains and the 17-19.5μ

MPG’s all moved closer to their previous highs set back in February rising 20-70c for the week. The offering

contained a growing percentage of low yielding, average style lots, but unlike the past sales the rises in the market

were kind to all style lots.

Merino Skirtings rose 25-50c with the finest lots with low VM drawing the most attention.

Crossbreds were in a different realm this week with a mixed bag of price signals straddling last weeks’ price levels,

and given the last month of solid rises in the crossbred sector this was a satisfactory result.

Cardings posted solid rises of 20-36c across the selling centres and there was some positive price signals on the

coarser crossbred cardings after a long period in the doldrums.

Southern Aurora Wool Report: – The auction market triggered better volumes in the forward with trades through to

June 2019. Modest volumes traded in the front months as growers were keener to take advantage of record levels

offered in the spring. The spike in the spot market delivered strong prices with August and September trading to

2010 on 19.0 microns and 1880 for 21.0 microns. With dry conditions still prevailing over most of the country

guaranteeing premium levels into the New Year seemed to be the focus for some growers. January 2019 traded at

1800 for 21.0 microns. Hopefully we will see the trend continue into next week allowing growers to achieve price

certainty over the coming season’s production.

The market gobbled up 97.7% of the 37,842 bales on offer this week with fleece lots passed in around 1% which has

to be some kind of a record. Reports were circulating the trade corridors that the purchasing was a replenishing of

stocks, as the global processors inventory were running dangerously low. This weeks’ result pushed the market levels

to 23% above the same time last year and has presented the Australian wool producers as the best market

environment in history.

Considering the forward offers in the front months (Spring 18) also hit new record price levels for those forward thinking producers wanting to secure income and justifying the elevated feed budget in the winter and immersed in an extended dry period across most production areas of the continent.

Wool remains the beacon of hope for a bright future for those who have persisted in wool producing sheep, and with 7 selling weeks remaining for the 2017-18 season, the value of wool sold this week – $75.65m – took the YTD sold value of wool at auction through to the $3bn mark ($3,003.81m). Extraordinary times where record prices have not only failed to attract more than 2% additional wool onto the market for the year, but the forward projection for wool production is at 1.7% reduction for the 18-19 season. Whilst we can never be certain about the longevity of the demand for our exquisite fibre, the fact that supply seems to be capped and will continue to have a major impact on the price of wool moving forward. It’s now the greatest time to be in Sheep and Wool. ~Marty Moses