Week 44:

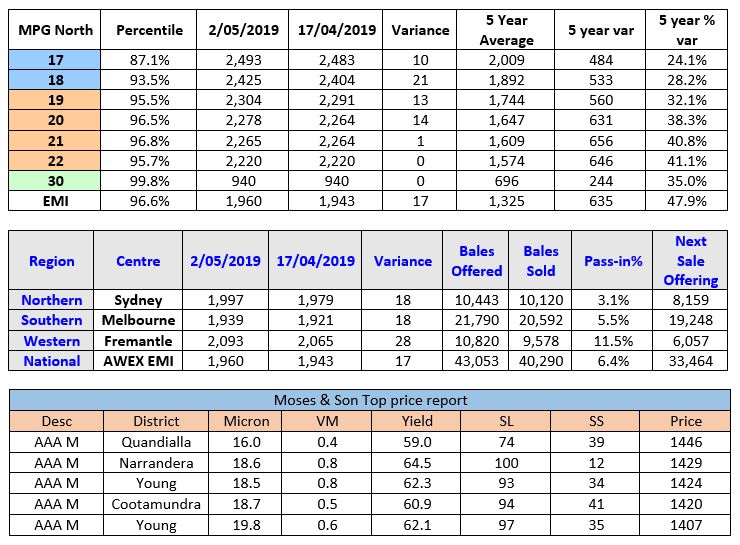

The AWEX EMI closed on 1960c, posting a 17c increase at auction sales in Australia this week. The 43,053 bale offering was met with some renewed interest from exporters after a weeks’ recess aided by the 1.7c drop in the AUD-USD exchange rate. The other factor in the exporter activity, was the next month’s sale roster forecast where the quantities drop off substantially with the cropping and pasture sowing period in full swing.

Merino Fleece experienced better competition, resulting in price increases between 5 and 20 dearer in the Northern markets and increases of 10-30c in the Southern region to further align them with the Northern MPG Premium. Best style and specified lots attracted noticeable premiums, whilst the poorly specified, dusty and drought affected fleece lots maintained previous price levels.

Merino Skirtings demonstrated two distinct paths; the best length and low VM lots increased in line with the fleece prices whilst the increasing quantity of shorter and heavy VM lots continued to feel the discounting.

Crossbreds are still enjoying heightened demand coupled with a diminishing supply, resulting in increases of 10-65c measured in the Northern markets and MPG’s smashing into new price record territory.

Merino Cardings had a small (10c) bounce this week after a 6 week losing streak.

Forward Price Report from Michael Avery (Southern Aurora Wool): The forward markets opened after the Easter Recess bid well on the back of a weaker AUD. This confidence translated into a stronger auction market in AUD terms (+17) but down in USD terms (-22). Most evident in the spot market, was the lack of participation of the usually dominant Chinese indent buyers. Demand is still sluggish and medium term off shore confidence is low. This is leading to the spring still being discounted and nearby months flat to cash.

Grower selling is only sporadic with the ongoing drought and production concerns clouding forward strategy decision making. 21.0 traded for June at 2250 near cash (2260) and October at 2125. This spring discount still places the price in the 80th percentile range of the last four years and reflects the current long-term view of the processors. We expect forward levels to remain solid with trading volumes again light. Sellers remain focused on the discount to cash rather than the outright level. Buyers are unable to commit to levels that the processors and consumers are still finding unpalatable. Evaluation of fair value remains difficult with the low drought induced supply balance the demand destruction that is inevitable with continued high prices. Increased forward flows will only come when both sides of the market value certainty above the fear of lost opportunity.

Commentary: Unfortunately the latest rainfall was extremely variable and not as widespread as it was first thought. Sadly, many districts are wondering when the next chance of moisture may arrive. Those who did get falls of some substance, the diesel will be burnt long into the nights as they race to sow crops and pasture for the upcoming season and hopefully a reprieve for the meals on wheels regime. One wonders what impact this not so general rain event will have on sheep and lamb prices and the already low wool production forecast reduction of -12.6% for Australia and -20% in NSW for the 2018-19 season and another 4.5% projected for 2019-20. The most telling statistic from the current season is the shift in micron profile year on year. For example wool tested finer than 16.6μ is up by 79% whilst the 21μ and 22μ are down by 41.4% and 40.9% respectively.

The question of “when is a drought over”? is one I have been pondering over, and it may start with an improvement in the feed situation pre winter allowing the feed cart to be parked, however, the financial, emotional and social impact of the event may be felt for many years to come. Michael Avery raises a very good point in relation to the expected performance of the market to deliver consistency in price out into the spring. Forward prices should be top of mind for most sheep producers who have invested heavily on carrying the stock through this difficult time. ~ Marty Moses