Week 52:

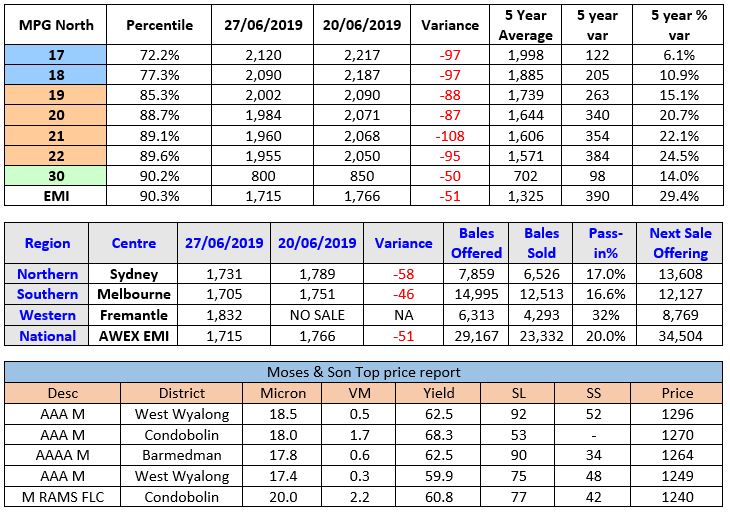

The AWEX EMI closed on 1715 – down 51c at auction sales in Australia this week. The free fall continues as exporters report a void in the confidence of any contracts being written with China and subsequently Europe and India. June measured the largest monthly fall (172c) in the EMI since March 1991, where the Reserve Price Scheme was abolished. One other possible contributor to the lack of interest in the weekly offering, was the stigma surrounding the last sale in the fiscal year.

Merino Fleece took another heavy hit with losses in the Eastern MPG’s ranging between 65c and 101c whilst the western MPG’s lost between 118c and 128c after a week’s recess in sales. The poorer style lots were more heavily discounted whilst the best style fleece lots were the subject of some moderate interest at reduced prices.

Merino Skirting prices played follow the leader of the fleece whilst the Merino Carding Indicator in the eastern states lost 24-32c whilst the closing Fremantle Carding market saw some support return with the western MC down just 9c.

Crossbreds were limited in their offering, especially in the Northern region but the low numbers did not create any demand so subsequently suffered losses of 30-50c.

Some statistics to ponder: Auction offerings fell 11.9%, or down 225,182 bales year on year, whilst the total value of wool sold at auction was $3,192.41M, or total $242.31M (-7%) down on last year sales total of $3434.72M.

Forward Price Report from Michael Avery (Southern Aurora Wool): Even in low supply, the poor demand and sentiment saw all merino qualities in the spot auction come off 80 cents. Selection of medium wools (21 and 22 microns) were so limited that AWEX were unable to provide a Micron Price Guide (MPG) quote in the Eastern States. The forward markets pre-empted this fall with both grower and trade selling early in the week.

19.0 traded 2045 for August pre auction but slipped to 1985 by weeks end. September and October traded early at 1950 but had fallen to 1900 by the close Thursday. The pattern in bidding and trading on the 21.0 contract was similar. Bidding in the early spring months around 1950 was ignored. December traded at 1900 to 1920 and closed bidding 1875.

Opinions remain divided on the length and depth of the current retraction. Major cycle times have varied from 6 to 12 months and the retraction from 20 to 40%. Fundamental indicators are hard to establish with exporters finding it difficult to write early spring/summer business. Processors remaining on the sidelines with concerns over the ongoing trade tensions freezing any action.

There is some speculative bidding in modest volumes. These levels indicate early stage support on 19.0 microns around 1870 to 1900 for September to December and 1850 to 1880 for 21.0 micron. These levels are 21% and 23% respectively under the peaks reach on those microns. 19.0 peaked at 2462 in August 2018 and 21.0 in February this year. A break of these levels would point to a deeper retraction.

From a percentile point of view, 1900 represents the 62nd level for 19.0 micron and 1880 the 74th level for 21.0 micron.

The difference (basis) between 19 and 21.0 is still predicted to remain tight. The current auction has 21.0 trading at a premium to finer microns due to the lack of supply. Forward bidding indicates that the fine wool premium will return with the better spring selection but will remain modest.

Commentary: There is no doubt the price slide is becoming more concerning week after week as the unresolved issue of the Chinese-US trade tariffs still sit on centre court for the world to view. It seems that on the eve of the G20 summit being held in Osaka, Japan, the stage is set for some resolution of this issue, but of course the risk of the tariffs being imposed in Chinese imports into the US either way will not be an easy fix. Unfortunately, the outlook for next week’s 34,504 bale offering is looking like “more of the same”. ~ Marty Moses